The genius of regular saving into KiwiSaver

George Soros, billionaire and famous investor once said, “If investing is entertaining, if you’re having fun, you’re probably not making any money. Good investing is boring.” (1)

Bolstered then by Soros’s quote, and supported by a lot of math, we embark on a discussion of the most “boring” but perhaps the most “good” of all investment techniques. That is…ready for it… a regular savings plan.

But why at a time like this would we talk about regular savings?

Flashback to the GFC around November 2008. The market had been going down for months and months. Investment banking firm Lehman Brothers was already bankrupt, and it looked like the entire financial system might crumble. My sister phoned me and said “Hey, at my work people are talking about suspending all their regular savings. Everything is just going down. Should I suspend my savings?”

My sister, like many fully employed people, was a regular saver. Money from each paycheck is directed into a saving scheme, relentlessly, religiously, buying, buying, buying.

Most employed people who sign up for KiwiSaver are in the same category. Every time they are paid, a portion of their salary goes into their KiwiSaver account. Through this mechanism they persistently purchase more and more shares each time.

Behind the scenes, there is absolute genius in this “boring” investment methodology, and it can only be truly appreciated when markets are volatile, either going down or up in price. So, what makes this such a powerful approach?

The Genius of boring investing

Let’s say that you are regularly contributing $1,000 a month into a savings scheme. When markets go down, that $1,000 per month purchases relatively more shares. When markets go up that $1,000 a month purchases relatively less shares.

That’s just obvious. But why would that be a form of genius? Well, think about it. You have just instituted a system that automatically buys more of something when prices are low and less of something when prices are high. That sounds like a good investment plan.

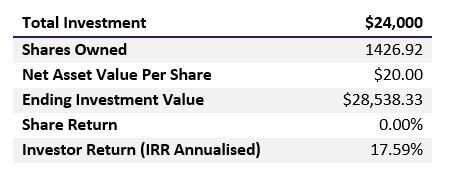

For those readers that are mathematicians or engineers, let me prove this to you mathematically. The table below is from one of the best investment authors of the past 20 years, Nick Murray (1). It highlights a market that over 24 months makes 0.00% return. However, over the first 12 months prices go down 30%, and then over the next 12 months prices recover back to where they started.

Most investors would look at such a market from start to finish as just treading water. But they’d be mistaken. To the regular saver, such a market has been a total success. By employing their technique of buying relatively more shares as prices fall and relatively less as prices rise, the regular saver has soundly beaten the market during the dip. Let’s trace what happens month by month.

Buying shares on ‘sale’

George Soros said that “good investing is boring“.

The shares started at $20 and finished at $20, so they clearly generated 0.00% return over 24 months. But the regular saver, who did nothing more than automatically invest their $1,000 a month, earned an internal rate of return (IRR, also known as money weighted return) of 17.59%.

The regular saver was able to purchase the greatest monthly quantity of shares at the lowest prices. For example, when prices (represented by the term Net Asset Value) had dropped to $14.00, the regular saver purchased 71.43 units. When the price was $20.00 the investor only purchased 50 units.

By the time the market recovered, those shares purchased at a price of $14.00 had strongly appreciated in value. In fact, by the end of the period, all the monthly share purchases were showing a profit, except for the shares purchased at $20, which were breaking even.

Once the regular saver catches on to the power of this methodology, their fears of volatile (or bear) markets should disappear, or at least reduce significantly. Nick Murray probably put it best when he said regular saving “makes you love – and long for – bear markets.”

For those of you that are investing in a KiwiSaver scheme, you are regular savers. This technique is at work for you right now, but only if you keep contributing. For a regular saver, the longer they can purchase shares at low prices they better off they’ll be in the long run.

Whilst this may seem a little “boring” just remember what George Soros said, “if you’re having fun, you’re probably not making any money.”

As for my sister, she continued to contribute into her saving scheme and did pretty well. I made a point to check on her balance a year later and she was up 45%. Her workmates, who 12 months prior thought it was a good time to stop their regular savings, hadn’t done anywhere near as well. When they looked at their respective balances, I’m pretty sure I knew who was having more fun!

1. George Soros, As quoted in The Winning Investment Habits of Warren Buffett & George Soros (2006) by Mark Tier, p. 217

2. https://www.amazon.com/Simple-Wealth-Inevitable-Revised/dp/0966976347

Are you interested in seeing how regularly contributing can impact your future KiwiSaver or investment balance? Please reach out to us today for a quick chat, or complete one of our quizzes below and we will be in touch to discuss your KiwiSaver or Investment options.

Compound Wealth are based in Mount Maunganui, Tauranga and offer KiwiSaver, Investment & Retirement Financial Advice to clients all over New Zealand.